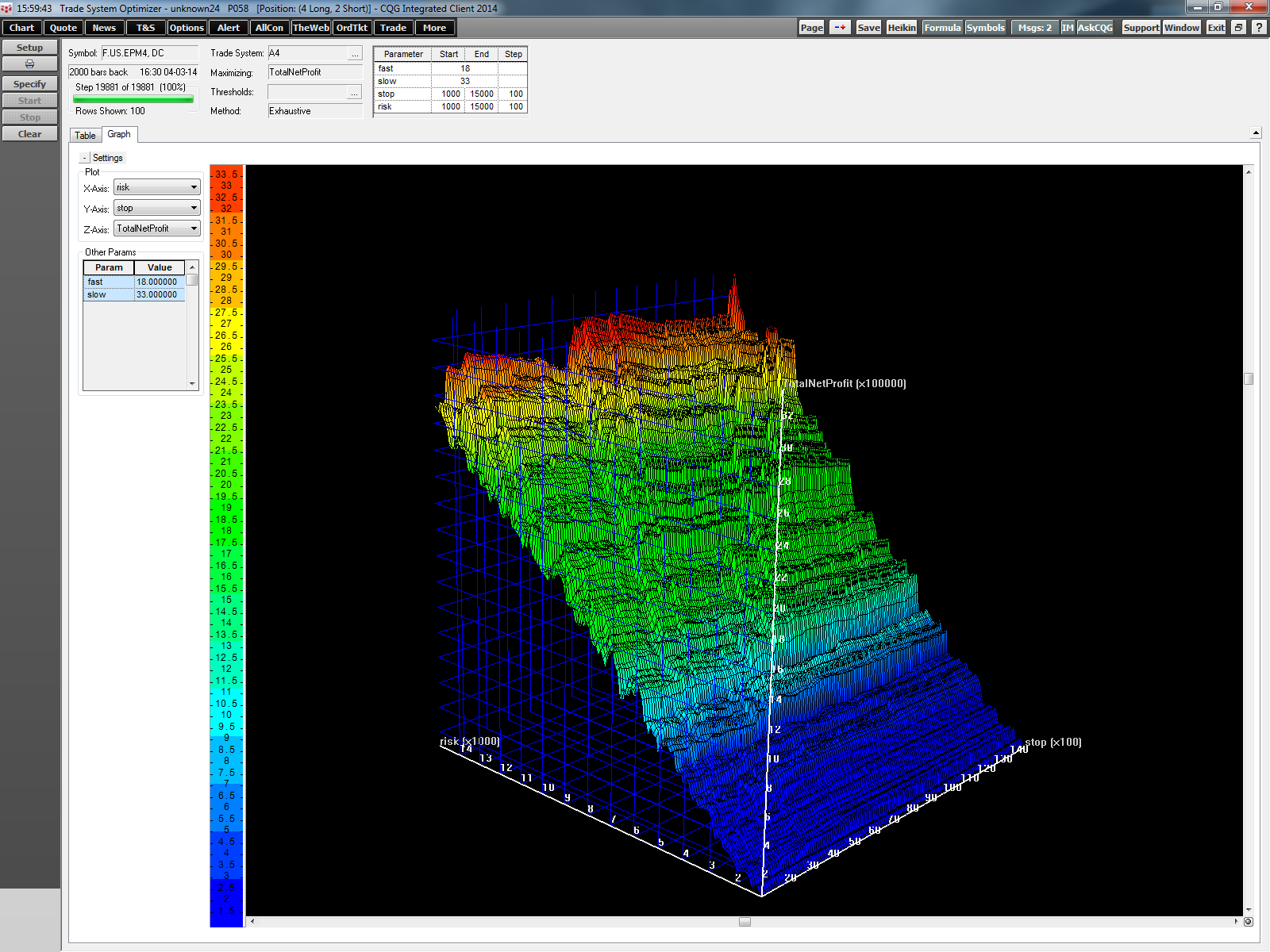

After we looked into some time frame considerations in my last article, the next logical question is to ask if CQG can "optimize time." CQG Trade System Optimizer (TSO) does not allow us to… more

Helmut Mueller

What is the right time frame for your trading?

Any data we analyze is more representative if we have a bigger number of samples. Asking ten people how the next elections will turn out will… more

One of my first backtesting tips featured a piece of code to limit a trading system only to one trade per day.

My colleague Doug came up with a smarter way to do this and even added the… more

One of the questions we received recently was if it is possible to trigger a trade in a certain market based on another trading system trading a different market. The answer is yes. Here is how to… more

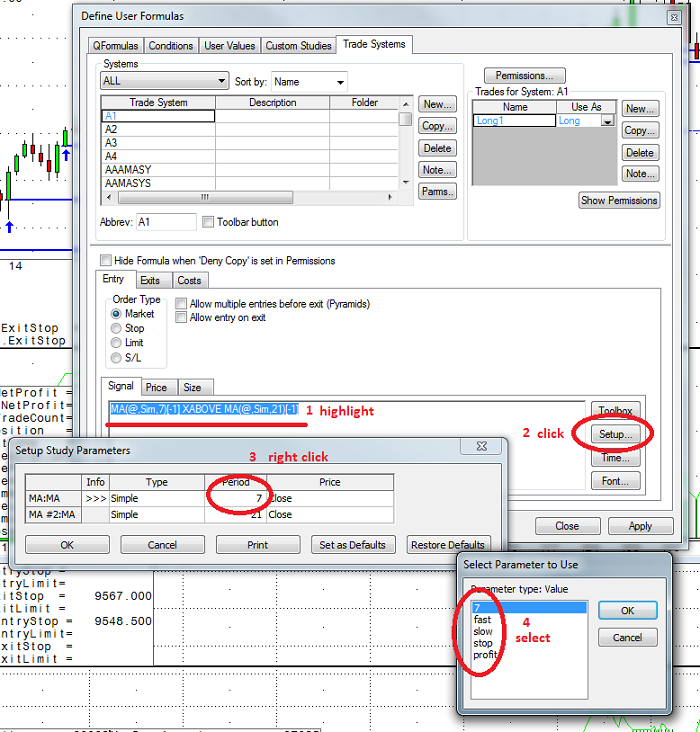

In my previous article, Backtesting Tip: Parameters inside CQG Code, I discussed the different parameter types and how to use them. This is important for all backtesting users because only values… more

We are getting a lot of questions about CQG parameters (Parms). In CQG, parameters are used for everything that needs to be controlled from the user interface and only Parms can be optimized.… more

The Peak-Ahead Problem

For most people the quick and dirty method of building trading systems using the signal bar closing price is good enough to judge a trading system… more

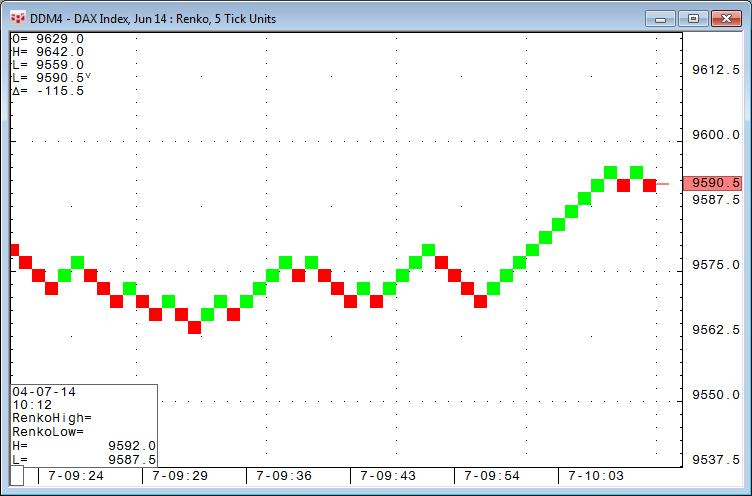

In CQG 2014 we will introduce three new chart types plus sub-minute bars, such as ten-second bar charts. In the next few articles we will have a short look into each one of them, starting with… more

In CQG Integrated Client version of the year, CQG 2014, we have introduced four new chart types: Heikin-Ashi, sub-minute bar, range bar, and Renko. In this article, we will look at… more