In systematic trading, the word robust is often used loosely. Yet robustness has a precise meaning to professional traders: a strategy's ability to survive regime change, parameter variation, crowding, and time. When comparing short-term swing models - such as those developed by Linda Raschke and Toby Crabel - to long-term trend-following systems associated with traders like Richard Dennis and Bill Eckhardt, the key distinction lies in the type of market inefficiency being exploited.

That distinction is best understood through the lens of tactical versus structural edges.

Two Different Sources of Edge

Markets are not inefficient in a single, uniform way. Instead, profitable strategies tend to draw from one of two broad categories:

- Structural inefficiencies, which arise from deep, persistent features of markets.

- Tactical inefficiencies, which arise from short-term behavior, constraints, and execution dynamics.

Trend following and swing trading sit on opposite ends of this spectrum.

Structural Inefficiencies: The Foundation of Trend Following

Trend-following systems - such as those popularized by Eckhardt - are rooted in structural market behavior. These behaviors persist because they are driven by forces that do not change quickly, if at all.

Key sources of structural edge include:

- Hedging pressure from commercial participants who must trade regardless of price

- Slow capital reallocation, as institutions adjust exposure over weeks or months

- Behavioral inertia, where investors underreact to new information

- Policy and macro shocks, which unfold gradually through positioning

Because these forces operate on long time horizons, trend persistence has been observable across asset classes and across centuries of price data. Importantly, trend systems tend to be parameter-robust: changing a breakout length from 20 to 55 days or a moving average from 100 to 200 days rarely destroys the edge.

This structural durability explains why trend following:

- Survives regime change

- Works across markets

- Produces positive skew

- Remains viable even when widely known

In short, trend following is robust because it exploits how markets are built, not how they are temporarily traded.

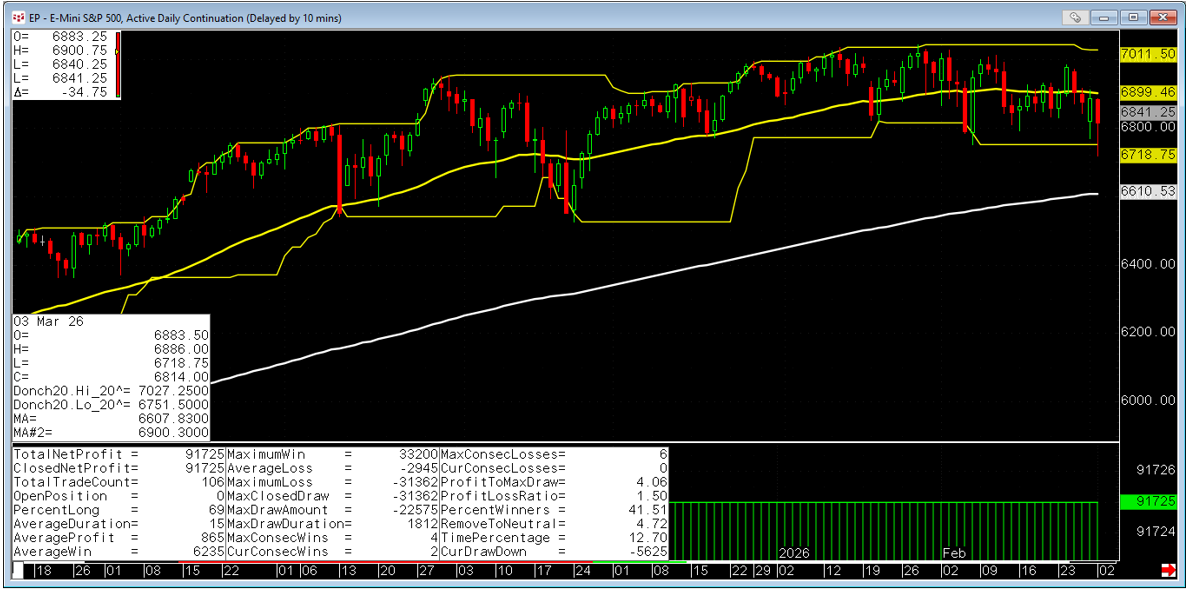

Here's an example of a simple trend-following model that combines Donchian breakout with moving average crossover (coding in CQG is shown below). Figure 1 (shown below) gives the backtested results of this model in E-Mini SP 500 futures:

Long Entry: High(@)[-1] > HiLevel(H,20,0)[-2]

AND MA(@,Exp,200)[-1] > MA(@,Exp,50)[-1]

Long Exit: Low(@)[-1] < LoLevel(Low(@),20,0)[-2]

OR MA(@,Exp,200)[-1] XBELOW MA(@,Exp,50)[-1]

Short Entry: Low(@)[-1] < LoLevel(Low(@),20,0)[-2]

AND MA(@,Exp,200)[-1] > MA(@,Exp,50)[-1]

Short Exit: High(@)[-1] > HiLevel(High(@),20,0)[-2]

OR MA(@,Exp,200)[-1] XABOVE MA(@,Exp,50)[-1]

Figure 1: Backtested results of trend-following model in E-Mini SP 500 futures.

Tactical Inefficiencies: The Domain of Swing Trading

Swing models developed by Raschke and Crabel operate very differently. Their edge does not come from slow institutional behavior but from short-lived distortions in execution and expectations.

Tactical inefficiencies arise because traders are:

- Constrained by rules

- Forced to trade at specific times

- Using similar risk management techniques

- Prone to predictable behavioral errors

These inefficiencies are real - but fragile.

Common Sources of Tactical Inefficiency

Volatility Compression and Release

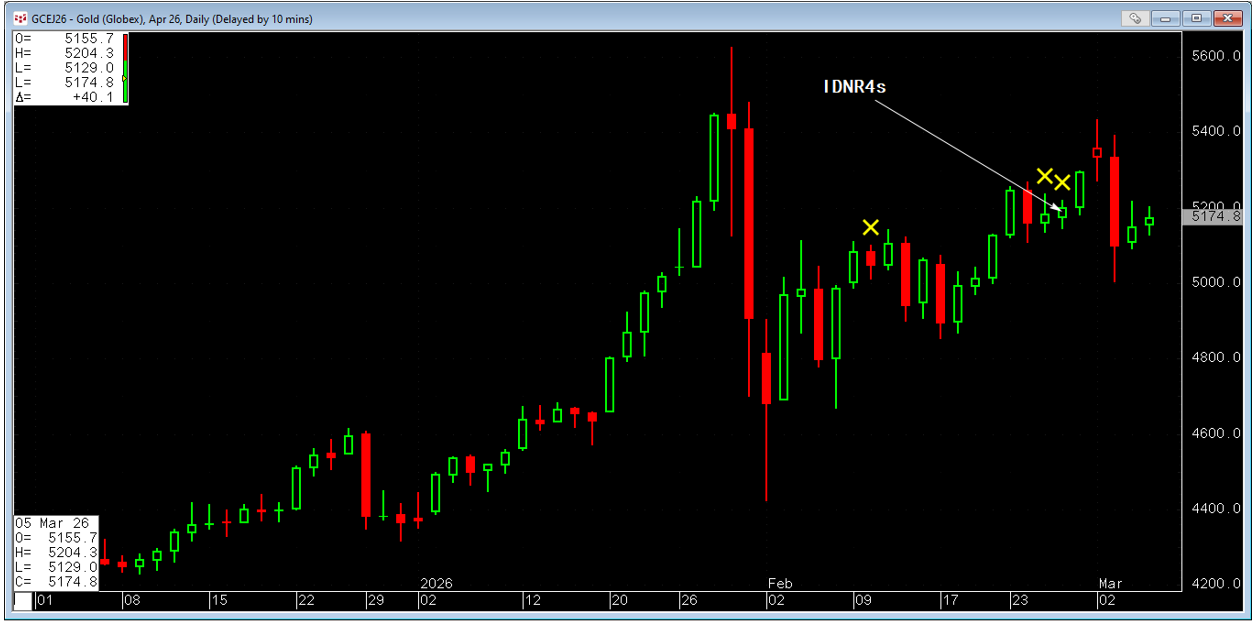

Crabel's Narrow Range and Inside Day patterns exploit periods of unusually low volatility. During these compressions, stops tighten and expectations converge. When price breaks, volatility expands faster than participants anticipate, producing brief but exploitable momentum.

Here's how to code Inside Day Narrow Range 4 as a "condition" in CQG:

(High(@) < High(@)[-1] AND Low(@) > Low(@)[-1]) AND

((High(@) - Low(@)) <= MinPrd((High(@) - Low(@)),4))

Here's some examples of IDNR4 (see figure 2 below):

Figure 2: April 2026 Gold with IDNR4s

Order-Flow Constraints

Funds rebalance, hedgers roll positions, and traders meet margin calls at known times. These flows can overwhelm liquidity temporarily, creating short bursts of directional pressure without implying a lasting trend.

Behavioral Anchoring

Many traders anchor to obvious reference points - prior highs, lows, or "fair value." When these levels fail, late exits and forced entries create asymmetric moves that swing systems attempt to capture.

Risk-Management Artifacts

The widespread use of ATR-based stops, fixed lookbacks, and similar volatility filters leads to stop clustering. Once these levels break, cascades occur - not because of new information, but because of mechanical risk exits.

Why Tactical Inefficiencies Are Less Robust

Tactical edges depend on how traders behave right now. As a result, they are vulnerable to:

- Crowding

- Parameter sensitivity

- Changes in market microstructure

- Shifts in volatility regimes

- Execution costs and slippage

This fragility is why swing models often require:

- More filtering

- More frequent adaptation

- Smaller risk allocation

- Continuous monitoring

Crabel himself emphasized that markets evolve and that short-term edges must be re-examined regularly. Tactical inefficiencies are opportunities - not permanent laws.

Comparison of Trading Approaches

| Dimension | Trend Models (Eckhardt) | Swing Models (Raschke / Crabel) |

|---|---|---|

| Edge Source | Structural: Relies on fundamental shifts and long-term momentum. | Tactical: Relies on short-term inefficiencies and price patterns. |

| Time Horizon | Medium to long | Short |

| Robustness | High: Tends to perform across various market conditions over time. | Moderate: Performance can be sensitive to specific market regimes. |

| Parameter Sensitivity | Low | High |

| Crowding Risk | Lower | Higher |

| Adaptation Needed | Minimal | Ongoing |

How Professionals Combine Them

In practice, institutional and sophisticated independent traders rarely choose one approach exclusively. Instead:

- Trend following serves as the core, providing long-term robustness and convexity.

- Swing models act as satellites, enhancing returns, smoothing equity curves, or providing diversification during trend-poor environments.

Risk allocation typically reflects this hierarchy, with trend systems carrying the majority of portfolio risk and swing systems occupying a smaller, more tactical role.

Conclusion

The key difference between Raschke/Crabel swing models and Eckhardt-style trend systems is not quality or intelligence - it is the nature of the inefficiency being exploited.

Trend following is robust because it feeds on structural features of markets that change slowly. Swing trading can be profitable because it exploits tactical inefficiencies created by human behavior and execution constraints - but those inefficiencies are inherently transient.

Understanding this distinction allows traders to:

- Set appropriate expectations

- Allocate risk intelligently

- Build portfolios that endure rather than merely perform

In the end, robustness is not about frequency or cleverness - it is about aligning strategy design with the kind of inefficiency markets reliably provide.