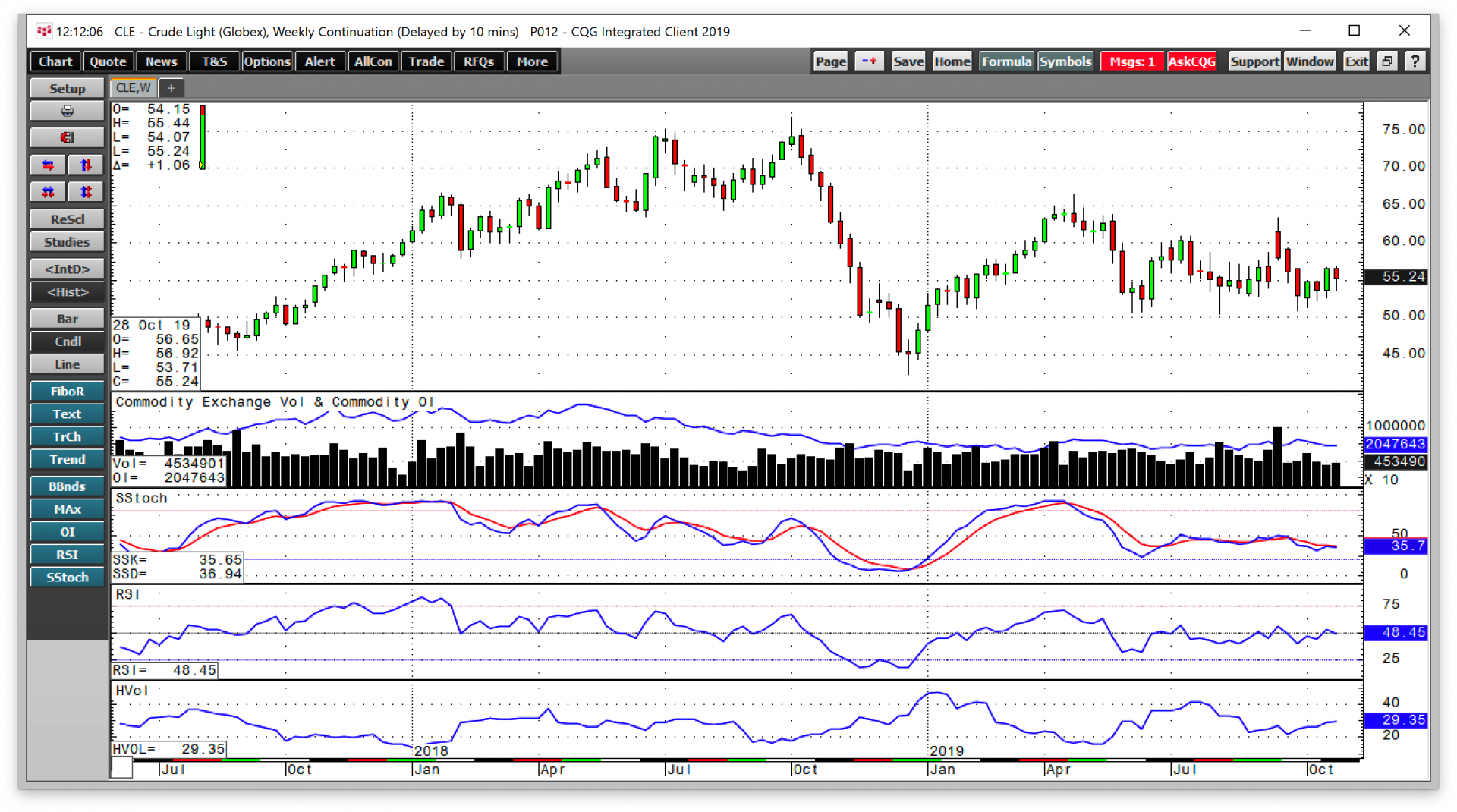

So far, in 2019, the price of nearby NYMEX crude oil futures has traded in a range from $44.35 to $66.60 per barrel. However, the low came at the very start of the year, and since the week of January 7, it has been at $50.52 per barrel.

Meanwhile, each time the crude oil market attempts to test the low, it fails at above $50 per barrel. On the upside, a drone attack on Saudi oilfields that temporarily knocked out 50% of the nation’s output, ran out of buying at $63.38 in mid-September. In 2018, the price of nearby NYMEX futures traded between $42.36 and $76.90. This year, the range has been far narrower.

The end of 2019 is approaching, which means the biannual OPEC meeting is coming. The cartel’s oil ministers, together with the Russians, will be gathering to decide on production policy for the first half of 2020. At the $55 level on nearby WTI futures and just above $60 on Brent futures on November 1, the members of the cartel will not be all that pleased with the current price of the energy commodity.

$50 has been significant support

It turned out that the price spike from $54.82 to $63.38 in nearby NYMEX crude oil futures from September 14 to September 16 was an outlier in the oil market. The price moved to the upside in the aftermath of the drone attack on Saudi production. With US output at 12.6 million barrels per day according to recent data from the Energy Information Administration, the rally in oil fizzled out quickly. Moreover, the Saudis returned production to pre-attack levels by the end of September, which weighed on the price of oil futures.

The price range in nearby NYMEX WTI futures has been from $50.38 to $66.60 since the week of January 7. If we ignore the price spike to the upside in mid-September as an outlier, the range has been from $50.52 to $60.94 since the final week of May. Each time the price ventured to the low end of the trading band, it found support. Price momentum was in the lower region of neutral territory at the end of October. Relative strength was sitting at a neutral reading. Weekly historical volatility was just below the midpoint of the year. At the same time, the total number of open long and short positions in the NYMEX futures market at 2.048 million contracts has been flatlining throughout 2019. The technical picture for crude oil is neutral, and the $50 level is critical technical support. NYMEX futures continue to face bullish and bearish factors that have kept the price of the energy commodity in a tight range.

The sweet spot for the Saudis on Brent is $60-$70 per barrel

In the lead up to the last OPEC meeting, the Saudis told the markets that $60 to $70 on Brent futures is a sweet spot for the energy commodity. As of the end of October, the price was sitting just above the bottom end of that range at $61.50 per barrel.

The Saudis, like all producers, would like to see the price of crude oil move higher from its current level. Balancing Saudi Arabia’s internal budget requires a price of oil at the $80 per barrel level on nearby Brent futures. At the same time, Crown Prince Mohammed bin Salman had been discussing the potential for an IPO of Aramco with financial institutions again in early September. The Saudis would like to sell a 5% interest in their state oil company to add to their sovereign wealth fund. In his Vision 2030, the Crown Prince outlined plans to diversify his economy away from dependence on oil revenues. Ironically, the investment funds to accomplish the goal must come from crude oil sales. The attacks on Aramco oilfields in mid-September threw more than a little cold water on the plans for an IPO, as in increased the risk premium for an investment in what would be the world’s most profitable oil company. The valuation of Aramco would also make it the publicly traded company with the highest market capitalization.

A higher oil price would increase the valuation of Aramco as the attack fades into the market’s rearview mirror.

OPEC in early December

The oil ministers of OPEC will gather in Vienna, Austria, on December 5-6 to establish production policies for the first half of 2020. While the members will meet on December 5, it will not be until the following day when the cartel will outline its plans. Russia has become a highly influential non-member of OPEC and has participated in output quotas to support the price of the energy commodity since 2016.

OPEC is likely to focus on the current price weakness in the oil market. The ongoing trade war between the US and China could cause the cartel to increase its production cut to a level that is higher than the current 1.2 million barrels per day. A further production cut and tighter output quotas could lift the price of oil in the aftermath of the early December meeting.

Politics will creep into crude and gas in 2020 in the US

Next year, US politics could play a significant role in price volatility in the oil market. The US is the world’s leading producer of the energy commodity and remains the top consumer. However, energy production is likely to be a topic of debate in the 2020 Presidential election. The incumbent President has encouraged crude oil and natural gas production with significant regulatory reforms. Technological advances in extracting energy commodities from the crust of the earth in the US have increased output. President Trump will run for re-election on a platform that continues his quest for energy independence and production that keeps the US in the leadership role when it comes to output.

On the other side of the political aisle, Democrats have embraced the “Green New Deal” that addresses climate change and fossil fuel production. Most opposition candidates competing for the party’s nomination support policies that would reduce the US carbon footprint the world. One of the leading candidates, Massachusetts Senator Elizabeth Warren, stated that she would ban fracking on day-one of her administration. The Presidential election will likely serve as a referendum on US energy production. As the world’s leading producer of oil and gas these days, a policy shift will impact not only fossil fuel consumption in the US but global supplies. If US production is going to decline under the “Green New Deal,” it could shift control of the energy markets and prices back to OPEC and give the cartel new life over the coming months and years. Oil-related shares have lagged the market in 2019, which could reflect the uncertainty of the future of production, refining, and logistics in the oil path because of political considerations.

Increased volatility on the horizon

Crude oil has been trading in a narrow range with support at $50 and technical resistance at around the $60 per barrel level on the nearby NYMEX futures contract. Natural gas at below $3 per MMBtu reflects inventories and production levels that are well above last year at this time.

Both of the energy futures markets remind me of rubber bands that are stretching as prices trade in narrow ranges. The more a rubber band stretches, the harder the eventual snap. We could see some wild volatility in 2020 in crude oil and natural gas markets. Buying options over the coming weeks and months before the 2020 election gets underway could be a low-risk and high-reward approach to the energy markets. 2020 is shaping up to be a year where price variance has the potential to be a lot higher than it in 2019.

Volatility can be a nightmare for investors, but it is a paradise for nimble traders with their fingers on the pulse of markets. Politics over the coming year could make that pulse erratic.