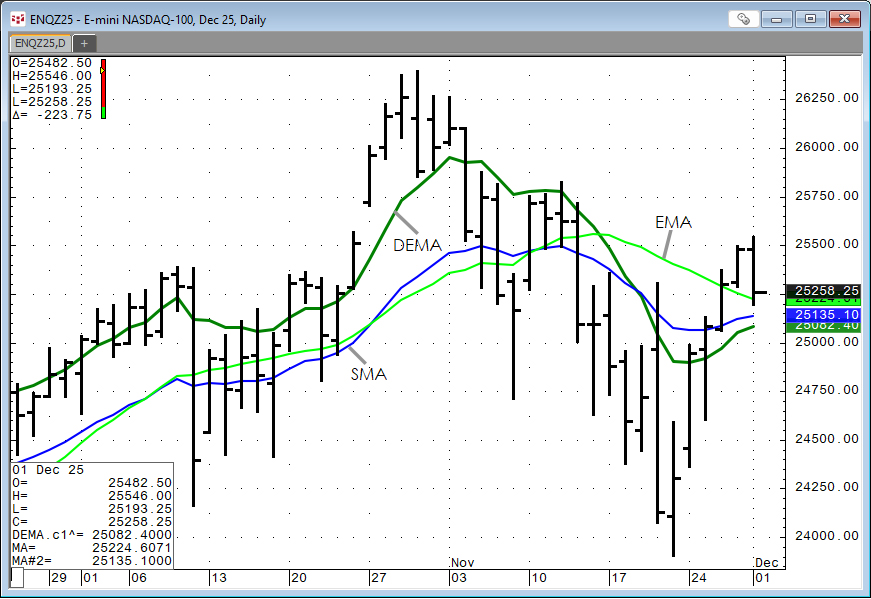

The Double Exponential Moving Average study is a moving average calculation that reduces the lag associated with other moving averages. The Double Exponential Moving average is calculated as the… more

Workspaces

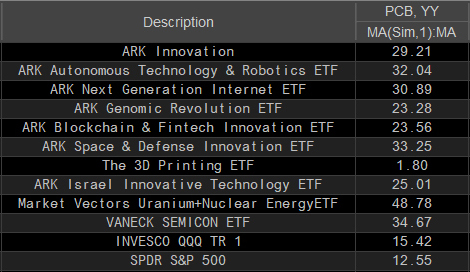

At the bottom of this post is a downloadable CQG Pac that installs a page for CQG IC and QTrader customers interested in following a section of the technology ETFs. The group of ETFs are displayed… more

From the ARK website: "Companies within ARKQ are focused on and are expected to substantially benefit from the development of new products or services, technological improvements, and advancements… more

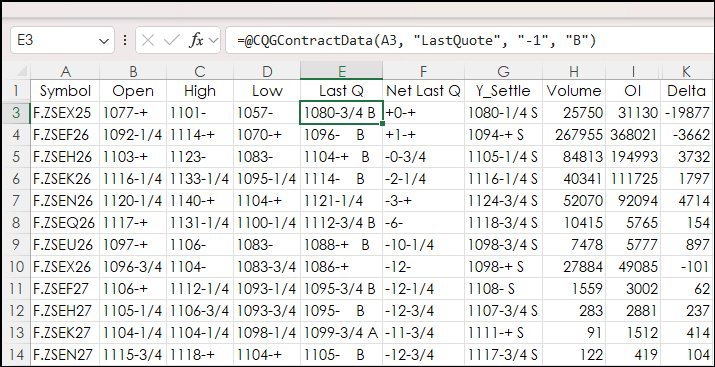

This post details steps using the Excel CQG RTD Toolkit Add-in to pull in open interest data for an options series based on the same expiration. These same steps can be used to pull in other… more

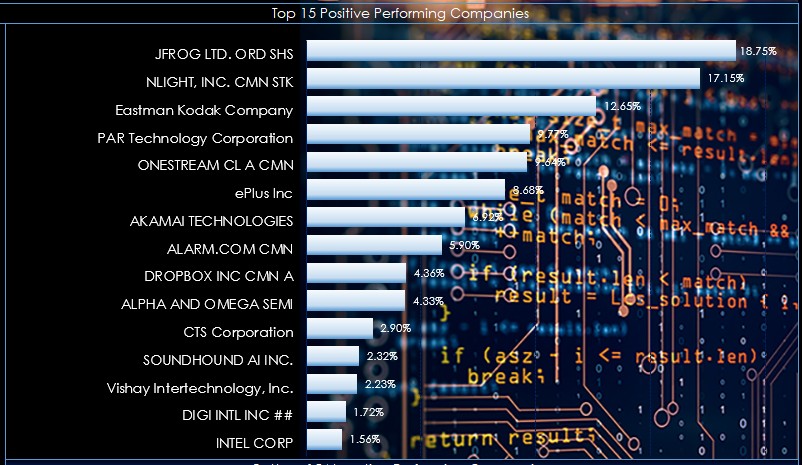

This post offers two Excel dashboards for tracking the holdings of the Vanguard Information Technology ETF. The fund tracks the performance of the CRSP US Large Cap Growth Index.

It uses a… more

This post offers a downloadable CQG PAC for IC and QTrader and Excel dashboard that includes two custom studies that track a market's performance by measuring the price difference between the… more

This post offers two Excel dashboards for tracking the holdings of the Vanguard Information Technology ETF. The fund tracks a market cap-weighted index of companies in the US information… more

CQG has added Commitment of Traders (COT) data for three Euronext Commodities. In the CQG Symbol Finder you can find "Euronext Commitment of Traders."

The three markets are:

CommodityCOT… more

A popular quote display for following a group of contracts in a particular commodity is the CQG All Contracts display. This post details the steps to replicating this display in Excel.

First… more

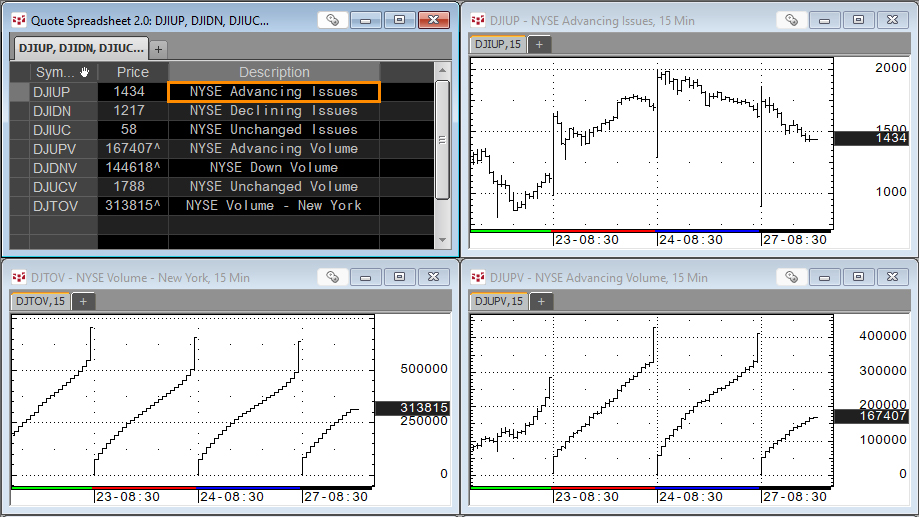

The CQG Comp group is a list of symbols that includes reports, indices, and cash markets. One group is the internal stats for the NYSE and NASDAQ Exchanges: the topic of this post.

This… more