The rally in the US Dollar that commenced in May 2014 continued to gain steam throughout much of the first quarter of 2015. The reserve currency of the world has an inverse relationship with commodity prices. In this piece, I describe how commodity markets mirrored action in the dollar during Q1, point out the winners and losers in the commodity markets, and explain why focus may now shift away from the dollar, fundamentals, and maybe even technical factors during Q2 and beyond.

The Dollar and Commodities

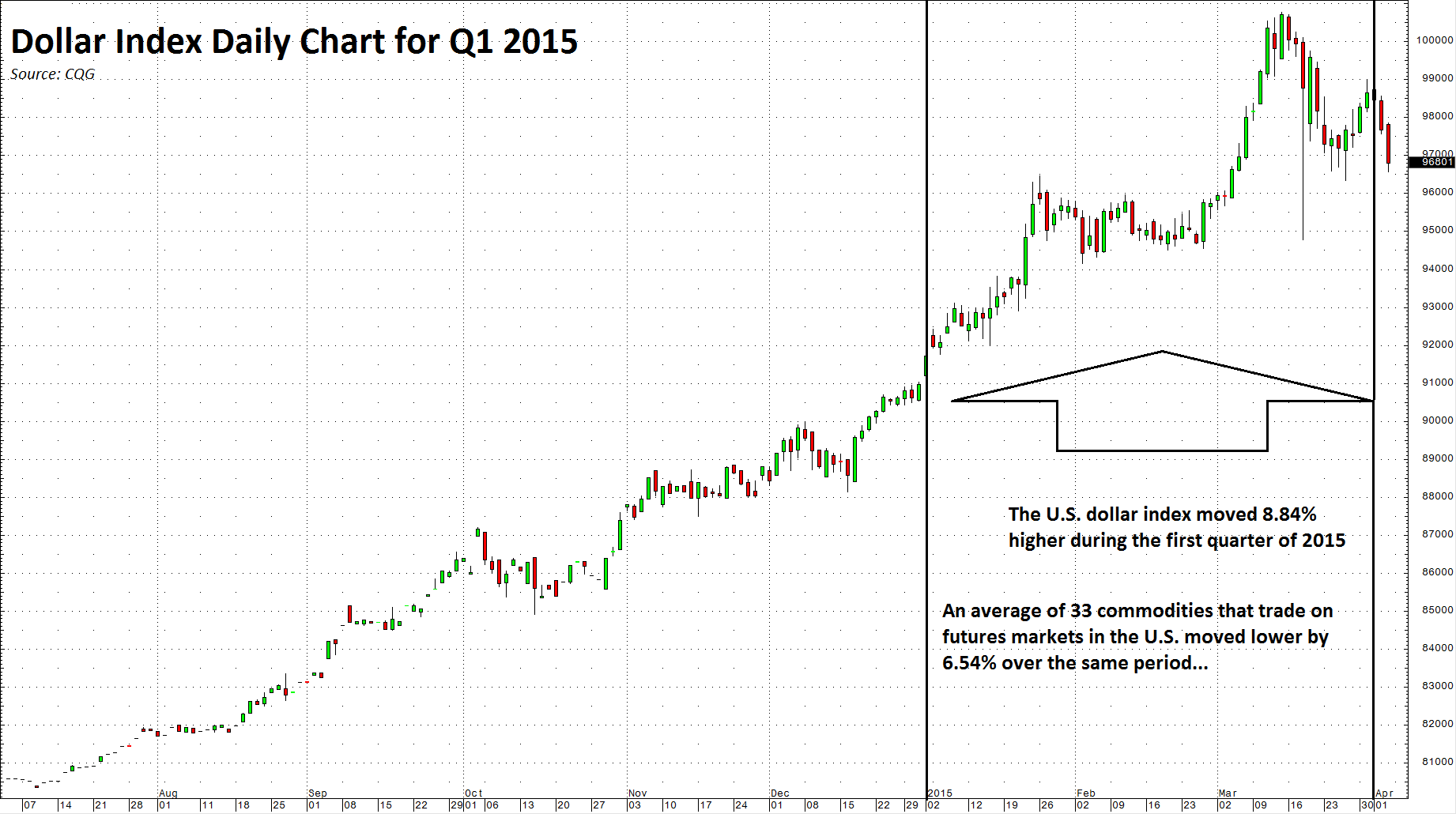

The dollar continued to be a winner during the first quarter of 2015 while most commodity prices moved lower.

As the chart illustrates, the dollar moved higher by 8.84% during the first quarter of 2015. Only after the Federal Reserve indicated that short-term interest rate hikes would come later rather than sooner did the dollar correct lower. However, the dollar index broke higher during Q1 taking out all long-term resistance levels, the last being the August 2003 highs at 99.57. Firm support now stands at the 96 level.

While the dollar moved 8.84 % higher, an average of 33 commodities traded on major commodity exchanges fell by 6.54% during Q1. The commodities include those from precious metals, base metals, grain, energy, soft commodity, and animal protein sectors. The action in raw material prices during Q1 once again validates the inverse correlation between the dollar and commodity prices.

Only a Few Winners in Q1

Commodities that appreciated in price during the first quarter are so few that I can count them on one hand. The best performer was gasoline, which was up 20.24%. Silver appreciated by 6.4% during the quarter, and cotton was up by 4.7%. That was it.

The big losers during Q1 were lean hogs, which dropped 23.13%; coffee, which lost 20.23%; sugar, which shed 17.84% of its value; nickel, which fell 17.24%; and CBOT wheat, which lost 13.23%. All other commodity prices lost value during the quarter. The score -- three up and thirty lower.

A Shift from Currencies to Geopolitics

While it is clear that the strong dollar had a huge influence on commodity prices in Q1, it is possible, maybe even probable that Q2 will be somewhat different. While both fundamental and technical factors often drive commodity prices, sometimes the biggest moves come because of world events. At the end of the first quarter, two world events could set the stage for lots of volatility during the second quarter of 2015 and beyond.

First, the agreement between the US and allies with Iran over their nuclear weapons program and sanctions could lead to changes in commodity markets. Iran is a major world producer of oil and new selling from the Iranians could change the fundamental equation for energy commodities. Moreover, there is a tremendous amount of conjecture about the agreement, which could lead to increasing volatility in raw material markets. Second, and perhaps more importantly, an expanding conflict in the Middle East, particularly in Yemen, has developed into a proxy war between Saudi Arabia and its allies in the Persian Gulf region and Iran who supports and arms rebels that overthrew the Yemen government. This could spell big trouble for the region if the conflict spreads in terms of not only production, but also logistics, as oil flows through certain choke points connected to Yemen.

These two events could mean big volatility for energy and other commodity markets as well as all assets in coming months.

Q2 - A Trader's Paradise

While the first quarter of 2015 saw commodity prices heavily influenced by the trajectory of the US Dollar, the second quarter is likely to provide other influences due to world events. Given the rapidly shifting geopolitical landscape, fundamental, and technical analysis along with currency moves could take a back seat to world events. This is a prescription for huge volatility in all asset classes, including commodities. Q2 may just turn out to be a trader's paradise because volatility is a trader's best friend.