The Inverse Relationship Could Mean the Next Leg Down

The US dollar is the reserve currency of the world. As such, it is the pricing mechanism for most important raw material markets. When the value of the dollar against other currencies moves lower, commodities become cheaper in those currencies, which encourages buying. When it moves higher, the opposite is true: raw material prices become more expense, which inhibits demand. During the cyclical bull market in commodities, which lasted from 2004 through 2011, the dollar remained weak.

In 2011, many commodity prices reached their peaks and since then they have been making lower highs and lower lows. Until 2014, the US currency remained stable and traded mostly below the 85 level on the US dollar index. Then in May 2014, the dollar began a rally that continues today.

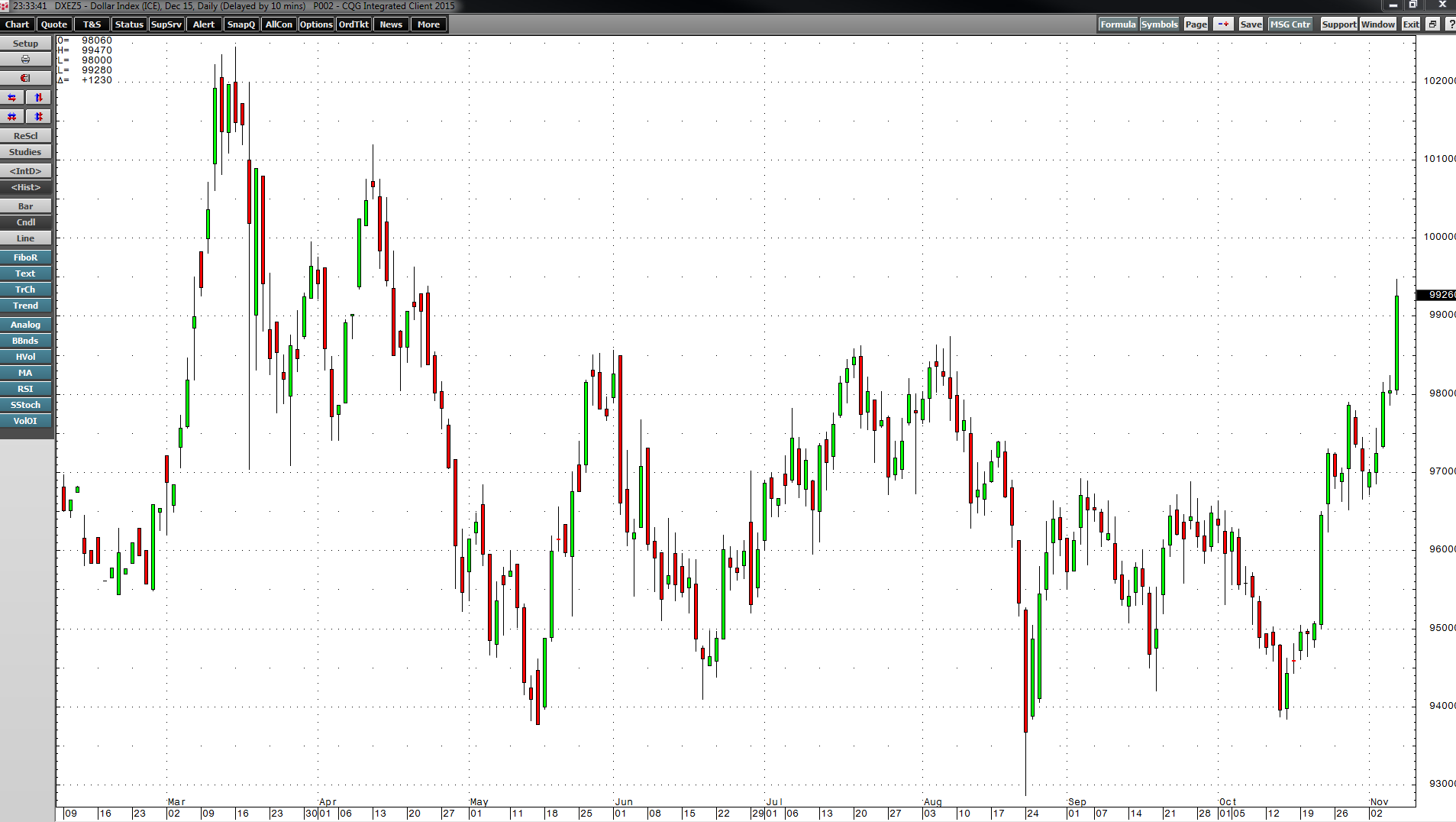

The Dollar is Back

A weekly chart of the US dollar index highlights the powerful move in the US currency since May 2014.

The move from lows of 78.93 to highs of 100.38 on the continuous contract took ten months. The more than 27% appreciation in the dollar caused problems for commodity prices, which had already been heading south. A combination of worsening fundamentals for many raw material markets and a stronger dollar caused selling in many commodities to accelerate.

After the dollar reached highs in March 2015, it consolidated and traded between just under 93 and just over 98 on the dollar index. Then, towards the end of October, the dollar started to creep higher. By the first week of November, the dollar broke out above the top side of the consolidated trading range.

As the daily chart illustrates, the dollar is back in bull mode. A combination of positive interest rate differentials between the dollar and other major currencies and stronger relative economic growth in the US provided fundamental underpinnings for the rally. Technically and fundamentally, the dollar appears to be heading for new highs on the current move. This is bad news for many commodity prices, which have been trading in bear market conditions for the past four years.

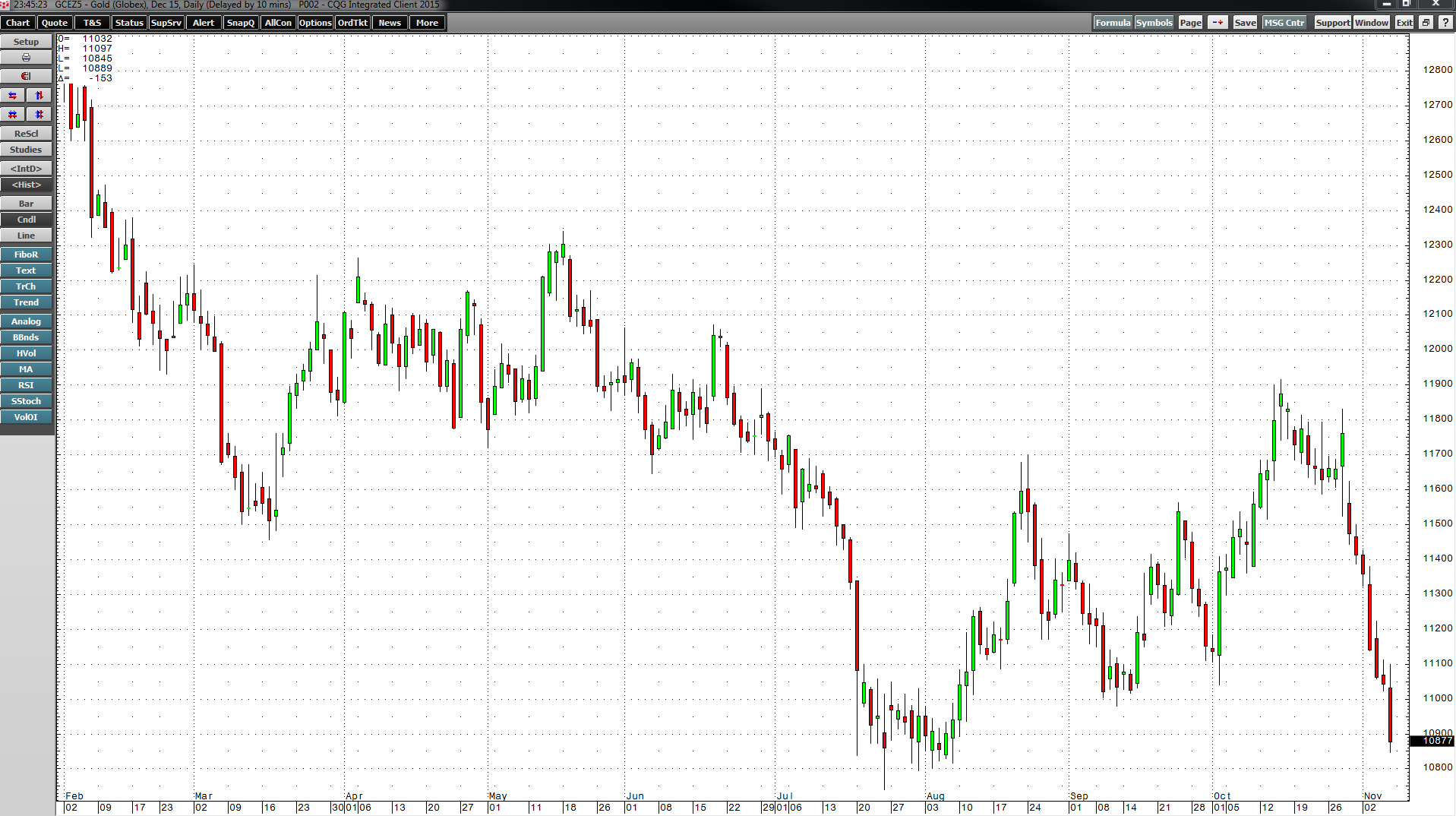

Gold Fails

The price of gold traded as high as $1920.70 in 2011, but has been falling since. In July 2015, gold hit another multiyear low when it traded at $1073.70 on the active month December COMEX futures contract. In the third quarter of 2015, gold posted a 4.83% loss and as of September 30, it was down 5.82% for the first nine months of 2015.

Over the first two weeks of October, the dollar moved lower and tested the bottom end of its trading range. During that period, a correction in gold took the yellow metal to highs of $1191.70 on October 15, the day the dollar index posted lows at 93.83. At the highs, gold erased all of the previous quarter's losses and was up marginally on the year. Key resistance at the $1234 level seemed within reach, but gold failed as the dollar turned around and took off to the upside. Since then it has been an uphill vacuum for the dollar and a very slippery slope for gold.

On Friday, November 6, gold closed at the $1089 per ounce level. Gold has now given back all of the recent gains and is now actually well below the level it traded at on September 30. Key support at the July lows is within a stone's throw.

Copper Looks to a Lower Low

While the price of gold has tracked the dollar well over recent weeks, the price of copper has been sensitive to not only the US currency, but also the economic conditions in China. The Asian nation is the largest copper consumer in the world and the economic slowdown has caused weakness in the red metal throughout 2015. Copper traded to highs of over $4.60 per pound in 2011; since then it has also been making lower highs and lower lows. The last low came on August 24 at $2.2025, the day that China shocked the world and announced a surprise devaluation of their currency, the yuan.

Copper attempted to rally over the first two weeks of October as the dollar moved to the bottom of its trading range but it only managed to increase from $2.341 at the end of September to $2.4375 on October 9. While gold rallied by 6.9% during the first two weeks of October, copper only managed gains of 4.1% before it ran out of gas. The red industrial metal closed on Friday, November 6 at $2.2420, just a few pennies above the August lows.

The Bottom Line

The dollar appears to have broken to the upside with more gains in store. This is bad news for gold and copper as well as other commodity prices. For these two metals, it looks like a continuation of bear market trading is in the cards with another new low on the horizon very soon.