Here is a special version of the Volume-Weighted Average Price (VWAP) study including standard deviation bands.

VWAP is the volume-weighted average price for a futures contract plotted as a line on the price chart. The calculation is the sum of traded volume times the price, divided by the sum of the traded volume.

This study has a number of uses. It provides the current volume-weighted average price for the trading day or the trading session. Traders can compare the current price to the VWAP. In addition, the VWAP can be calculated using a set look-back period to smooth the price data similar to a standard moving average.

VWAP = (Sum of traded volume*price)/(Sum of the traded volume)

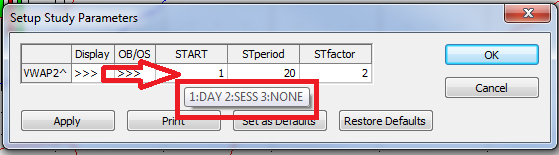

The parameters are as follows:

- START: VWAP starting point 1=Start of Day, 2=Start of Session, 3=None

- STperiod: length of the standard deviation calculation

- STfactor: factor of the standard deviation to be added or subtracted from the VWAP

File